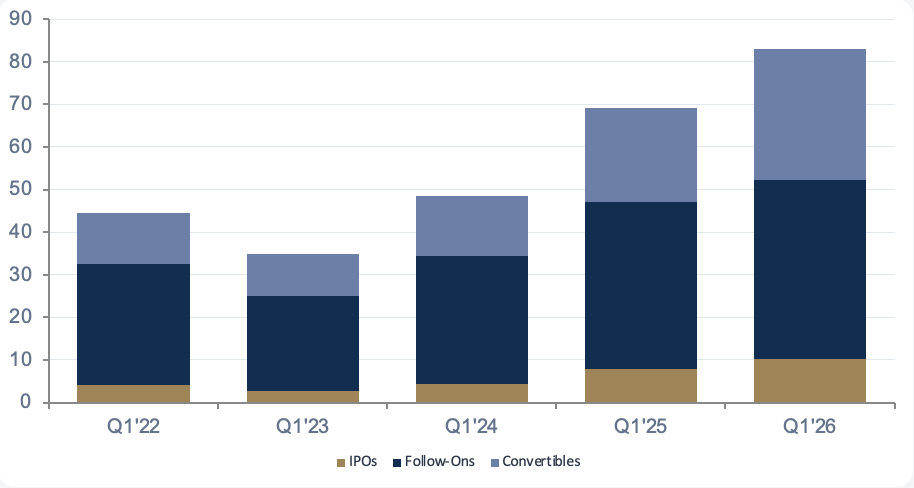

Equity Capital Markets Update: The Strongest H1 Issuance Pace Since 2021

U.S. equity issuance has topped $120B year-to-date — the strongest first-half pace since 2021 — as AI-infrastructure IPOs, sponsor-driven follow-ons, and a record run of convertibles redefine the market. With the Fed succession resolved and earnings the strongest in four years, the H2 window looks constructive — though a fragile Iran ceasefire and elevated oil cap the upside.

By ArcStone Financial Pulse

Published June 2026 · 7 min read

READ THE FULL REPORT HERE:

U.S. Equity Capital Markets

A $120B+ Year-to-Date Snapshot

| $120B+ | $42B+ | $37.6B | $34B+ |

|---|---|---|---|

| Total ECM proceeds | Follow-ons (Q1) | IPOs · 63+ deals | Convertibles (thru Apr) |

U.S. ECM proceeds have topped $120B YTD — up roughly 50% versus the H1 2025 pace and the strongest first-half run since 2021. Follow-ons led with $42B+ in Q1 (predominantly sponsor monetization, ~51% of Q1 proceeds), while IPOs have raised $37.6B across 63+ deals — already approaching full-year 2025's $44B. Convertible issuance is running at roughly 2x last year's pace ($34B+ through April), anchored by Oracle's $5B mandatory convertible preferred and CoreWeave's $4B deal. AI infrastructure has established a new thematic lane — Cerebras at $5.55B, Fervo at $1.89B — though that concentration introduces fragility if AI sentiment shifts.

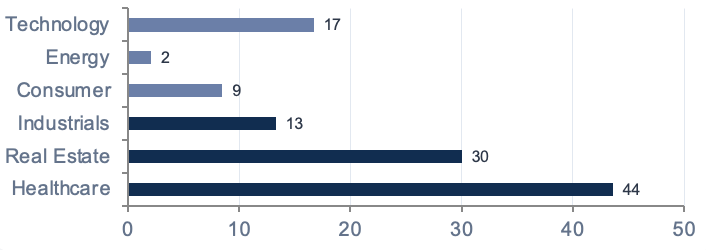

U.S. IPO Market

Sector Breakdown: AI/Tech and Healthcare Lead

The IPO pipeline is the deepest since 2021, and the market is now clearly differentiating. Healthcare anchored Q1 with 7 deals and +43.6% average returns (6 biotech IPOs versus just 7 in all of 2025), but rotated to -6.2% YTD in Q2 as capital moved to AI. Technology staged a dramatic reversal — +16.7% YTD after -5.8% in Q1 — led by Cerebras Systems' $5.55B IPO on May 13, the largest AI-chip IPO ever. Industrials carry the AI-power nexus: Forgent Power ($1.5B) and Fervo Energy ($1.89B) reflect a world structurally short on electricity, underscored by NextEra's $67B Dominion acquisition. Financials were absent in Q1, but Kraken and Plaid (~$8B) sit in the Q2/Q3 pipeline.

Follow-Ons, Secondaries & Convertibles

The Real Volume Drivers

| $20.3B | 67% | ~50% |

|---|---|---|

| Q1 secondary volume | March follow-ons sponsor-led | of converts AI-linked |

Beneath the IPO headlines, follow-ons and convertibles are doing the heavy lifting. Q1 follow-on proceeds reached $42B — with sponsors an estimated 67% of March volume, as vintage 2017–2020 PE funds press for LP liquidity. Secondary selling now rivals primary raising: $20.3B in Q1, including $13.3B in March alone. Convertibles continue at ~2x the 2025 pace, and roughly half of issuance is AI-linked. In our view, issuers are locking in favorable terms while the VIX sits near 16.76 and the 10-year has pulled back to 4.59% — conditions that may not persist if the Warsh Fed signals a more restrictive posture.

Alternative Pathways · SPACs

SPACs: Quality Bifurcation Accelerates

| ~80 | 352 | 111 | 11 |

|---|---|---|---|

| SPAC IPOs (thru Apr) | Active SPACs | Pending de-SPACs | Closed YTD |

Roughly 80 SPAC IPOs through April raised ~$14B — a near-4x surge versus the same period in 2025 — but this cycle is concentrated among institutional-grade sponsors with performance-based promotes and committed PIPE financing, aided by the SEC's 2024 IPO-grade disclosure reforms. The pressure is acute: of 352 active SPACs with 111 pending de-SPACs, only 11 have closed YTD, with redemption rates above 95%. ArcStone estimates 25–35% of active vehicles will extend or liquidate as ticking trust clocks widen the gap between institutional-grade and speculative SPACs.

Canadian Capital Markets

Canada: The CPC/RTO On-Ramp

| $12.22B | 2,600+ | 86% | 3–5 mo |

|---|---|---|---|

| TSX/TSXV raised (+100%) | CPCs since 1986 | CPC completion rate | CPC/RTO timeline |

Canada raised $1.54B across 19 IPOs in 2025 (the TSX carried 99% of dollar volume), but the country's distinctive engine is the CPC/RTO route. With 2,600+ CPCs listed since 1986 and an 86% lifetime completion rate, a reverse takeover into an existing shell can close in 3–5 months versus 6–9 for a traditional IPO — offering founders certainty of listing and a built-in shareholder base. Private placements and flow-through shares remain the dominant financing tools on the TSXV, particularly for resource issuers. A Canadian listing can also open a U.S. cross-listing pathway in roughly six weeks. TSX and TSXV raised $12.22B through April (+100% YoY), with the TSX Composite at 34,257 (+7.1% YTD).

Macro Backdrop

Forces Shaping the H2 Window

Four forces define the H2 landscape. Trade: the U.S.–China framework (U.S. ~30%, China ~10%) has cut tail risk, but the Iran ceasefire is fragile and Brent holds at $104.72. Fed: Warsh's May 13 confirmation resolved succession uncertainty; with funds at 3.50–3.75% and the 10-year back to 4.59% from a 4.92% March peak, markets are pricing 'higher for longer' rather than fearing the unknown. AI supercycle: ~$725B of 2026 hyperscaler capex — with power, not compute, the binding constraint — is reshaping issuance. Earnings: +27.7% Q1 EPS growth (84% beat rate) underpins both sponsor exits and primary issuance, though peak earnings growth often coincides with peak ECM activity.

H2 2026 Outlook

A Scenario Framework

Probabilities reflect ArcStone's subjective assessment, not model-derived forecasts.

| Scenario | Prob. | Trigger | Implication for ECM |

|---|---|---|---|

| Bull | 35% | Iran ceasefire holds, tariff truce broadens, Warsh signals continuity, AI monetization accelerates | IPO market reopens broadly — 60+ U.S. deals, $55–65B annual proceeds; AI-infrastructure anchors the calendar; TSXV/TSX surge |

| Base | 45% | Managed volatility: Iran stalemate persists, tariffs steady, Warsh holds, earnings stay strong | ECM front-loaded into windows; healthcare and industrial/AI IPOs dominate; converts elevated; SPAC quality bifurcates |

| Bear | 20% | Exogenous shock: Iran re-escalates, Warsh pivots hawkish, tariff truce collapses, earnings miss | IPO market freezes as in H1 2022; SPAC extension/liquidation wave; Canadian resource plays hit hardest |

Strategic Implications

What It Means for Issuers, Sponsors & Investors

- IPO readiness is non-negotiable. The backdrop is favorable, but windows can compress rapidly — Cerebras filed ~18 months before its May IPO, illustrating the lead time required.

- Sponsors: be surgical on timing. The most constructive exit backdrop since 2021; AI-infrastructure and power-adjacent names attract the strongest multiples, while others may favor secondary blocks or continuation vehicles.

- Canada's CPC/RTO is underutilized. For sub-$150M issuers, the TSXV route — plus a U.S. cross-listing pathway in ~six weeks — offers speed, cost efficiency, and a deep mining/cleantech investor base.

- AI infrastructure is the dominant theme. ~$725B of hyperscaler capex is directing capital to data-center power, critical minerals, and cooling on both sides of the border — with real concentration risk.

- Convertibles: act before the window closes. VIX near 16.76 and the 10-year at 4.59% have created favorable pricing; historically, convertible windows tighten as rate uncertainty resolves.

- Investor selectivity is permanent. Selectivity is a quality filter, not a closed door — scale, AI relevance, and clear profitability earn premium valuations; names lacking them face a tougher reception.

About ArcStone Capital Markets Advisory

ArcStone brings institutional-grade equity capital markets advisory to growth companies, sponsors, and boards across New York, Miami, Dallas, and Toronto — spanning IPOs, follow-ons and secondaries, SPACs, convertibles and hybrids, Canadian CPC/RTO transactions, and cross-border U.S.–Canada listings.

Disclaimer.

This publication is general market commentary prepared by ArcStone Financial Pulse Inc. (“AFP”), a subsidiary of ArcStone Securities and Investments Corp. (“ArcStone”), for informational purposes only. It discusses broad equity-capital-markets conditions and trends; it is not investment, legal, tax, or accounting advice, is not tailored to any person’s objectives or circumstances, and is not an offer or solicitation to buy or sell any security.

The market data, statistics, and figures cited (including issuance volumes, deal counts, index levels, rates, and transaction details) are drawn from public filings, exchange data, and other third-party sources believed to be reliable but have not been independently verified by AFP; they are stated as of the date of publication and are subject to change. Companies, securities, and transactions are named only to illustrate market trends and do not constitute a recommendation, endorsement, or rating, nor do they imply any relationship between AFP and the named party.

Statements regarding the H2 2026 outlook, and the Bull/Base/Bear scenario probabilities, are forward-looking and reflect AFP’s subjective views and assumptions as of the date of publication. They are not forecasts, guarantees, price targets, or earnings estimates; they are subject to risks and uncertainties that may cause actual outcomes to differ materially; and they should not be relied upon as a basis for any investment decision. Past performance is not indicative of future results.

AFP is not a registered broker-dealer or investment adviser. AFP is under common ownership with, and shares personnel with, registered broker-dealers (including ArcStone Securities, LLC, Member FINRA/SIPC), which creates potential conflicts of interest. This publication is editorial commentary, not equity research, and is not a research report within the meaning of FINRA Rules 2241 or 2242. Readers should conduct their own due diligence and consult their own advisers before acting.